Multifamily Boom: Hype or Not? Five Market Indicators We're Watching

Multifamily Boom: Hype or Not? Five Market Indicators We're Watching

Anna Duan, Geospatial Data Scientist

0. Introduction

The rental market hasn’t looked this strong in years and the industry is buzzing about a possible multifamily boom. At a recent John Burns real estate summit, bullish views outnumbered doubts five to one. CBRE is calling 2025 a “multifamily resurgence”, pointing to a sharp reversal of post-pandemic trends.

At Forty5Park, we put those bold claims to the test. Using our own data alongside open-source benchmarks, we find real momentum but also a more complex story than the headlines suggest.

In the next five sections, we break down the datapoints we’re watching most closely and discuss what they reveal about whether a multifamily boom is coming.

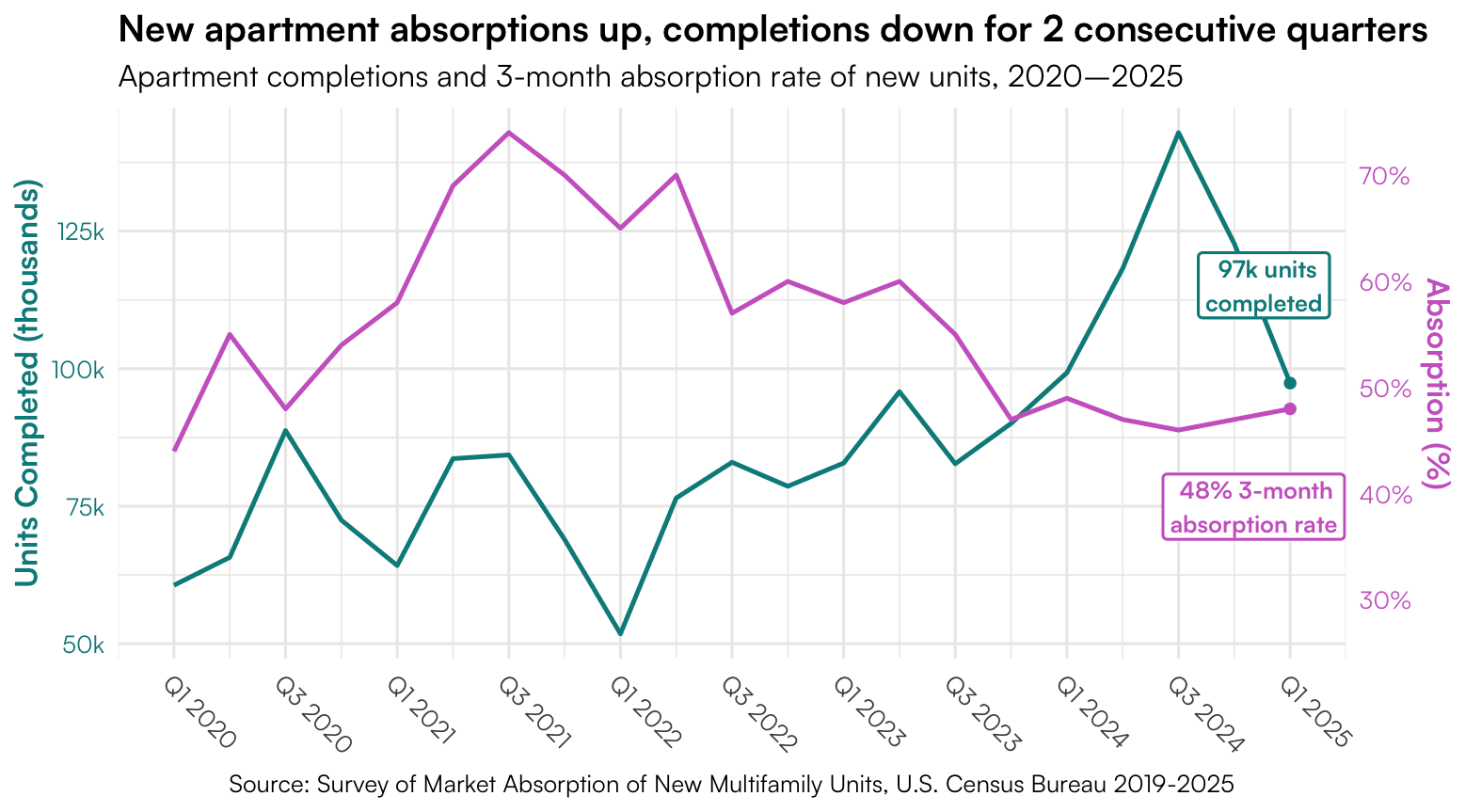

1. Rising Absorption

The centerpiece of multifamily optimism is this year’s record-breaking absorption. In Q2 alone, 188.2k units were absorbed: 44% above the pre-pandemic average, according to CBRE. Q1 wasn’t far behind, with 100.6k units absorbed, the strongest first quarter since 2000 (Multifamily Executive).

New construction is also showing encouraging signs. The Census Bureau’s Survey of Market Absorption (SOMA) tracks how quickly new units lease up. The chart below shows that after three years of decline, the 3-month absorption rate has now risen for two consecutive quarters. This means that as of Q1, 48% of newly completed units are rented within 3 months. At the same time, completions have fallen for two straight quarters and may undershoot demand for the first time in two years—a shift that could tighten the market further.

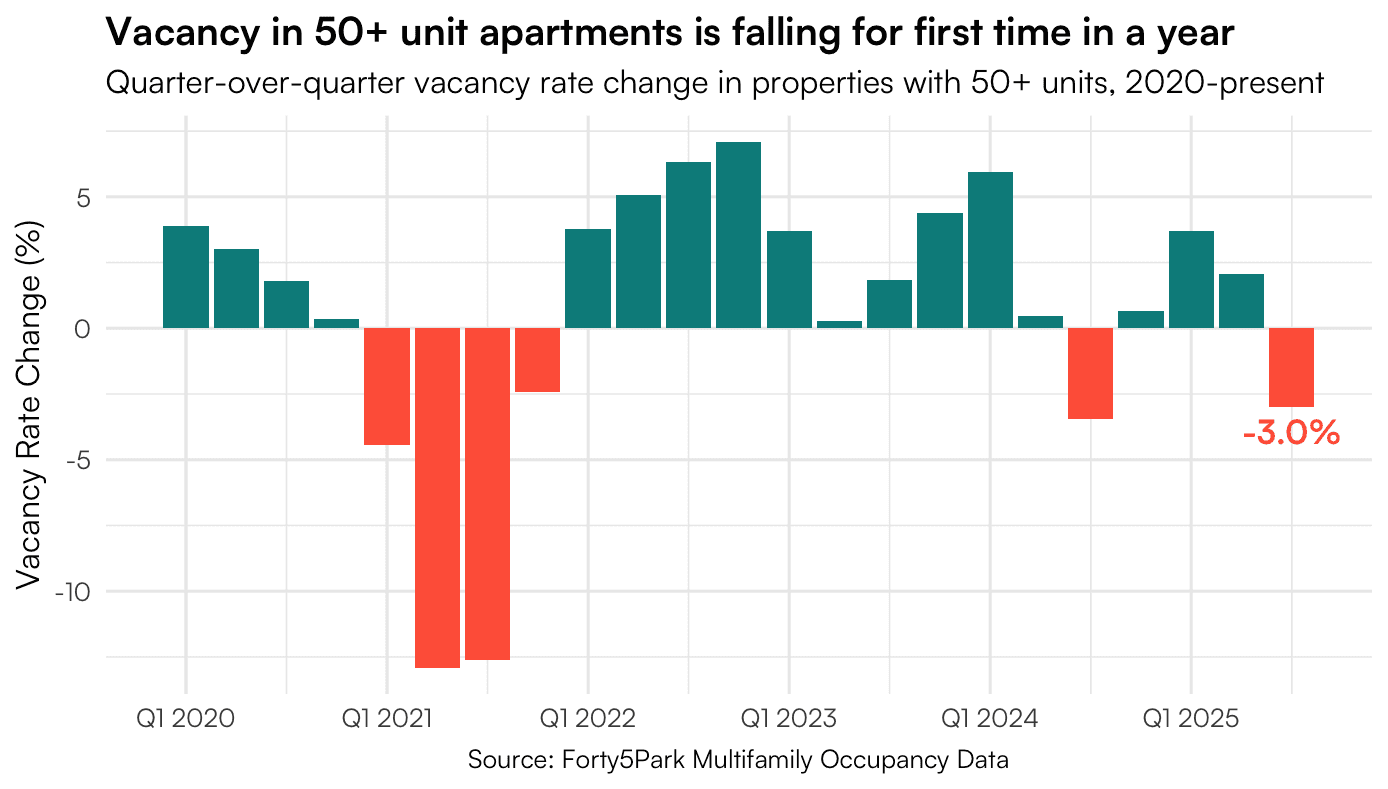

2. Falling Vacancies

Vacancies are tightening nationwide. CBRE reports the national multifamily vacancy rate has fallen to 4.1%, well below the long-term average of 5%. Our internal analysis of properties with 50+ units shows a higher vacancy of 6.2%. Still, that figure marks a 3% drop in Q3 2025, the first quarterly decline in a year.

With demand outpacing completions for five straight quarters (CBRE, U.S. Census Bureau), the tightening vacancy trend is likely to accelerate, putting upward pressure on rents and reinforcing investor confidence.

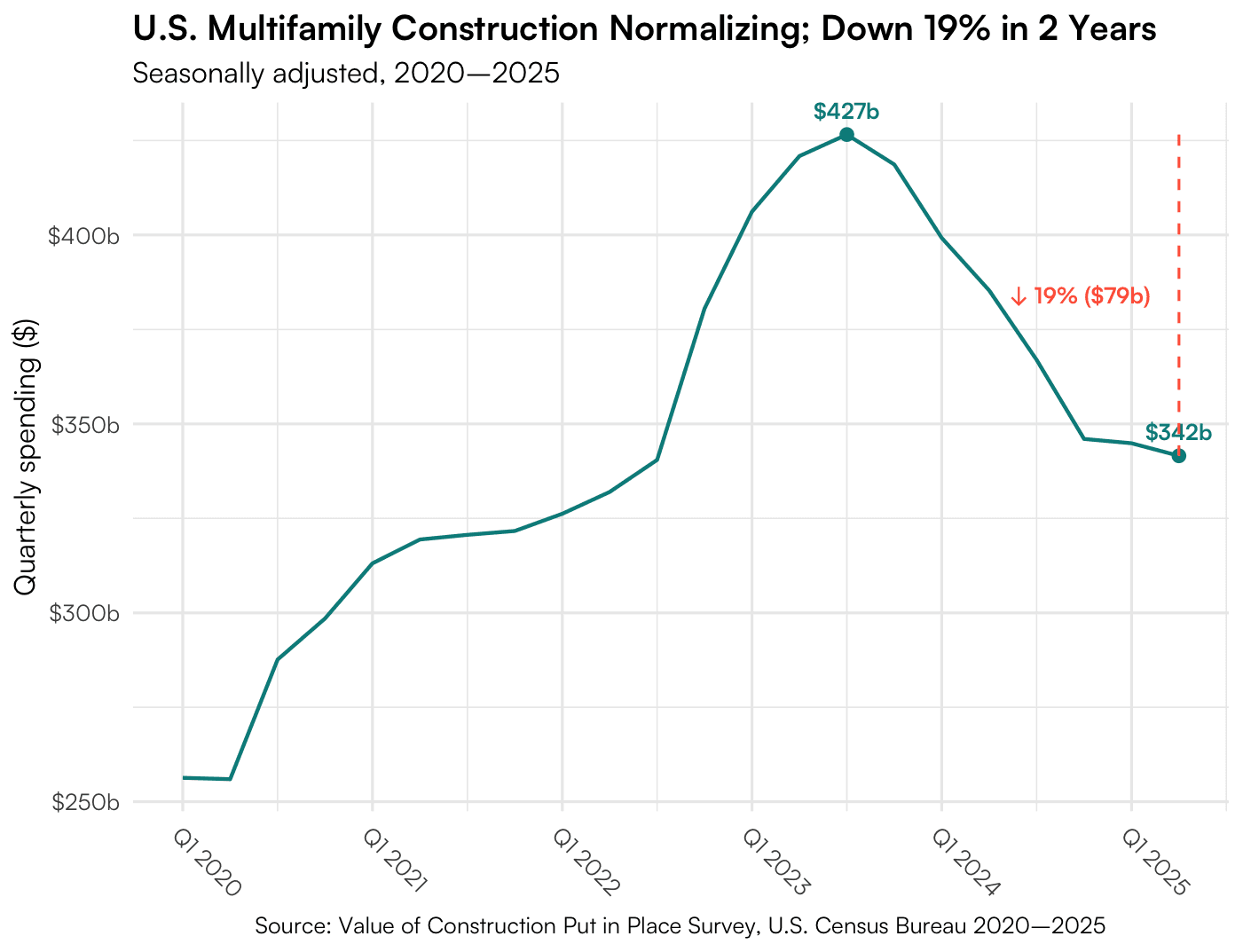

3. Supply pullback

After years of oversupply concerns, the market is shifting. While 2024 delivered a record 450k new units, Q2 2025 completions dropped to just 83k.

The pipeline reinforces the trend. Multifamily starts have fallen sharply from their 2021 peak and are projected to be 74% lower by mid-2025 (CBRE). Permits and construction spending are also sliding from 2022–2023 highs: Census data shows a 19% drop in multifamily construction spending since 2023, with permits showing similar declines.

This pullback comes at the right time. Absorption has consistently outpaced new deliveries, creating a 58% gap between demand and supply: the widest since the immediate post-pandemic recovery (CBRE). That imbalance sets the stage for faster lease-ups and potential rent growth ahead.

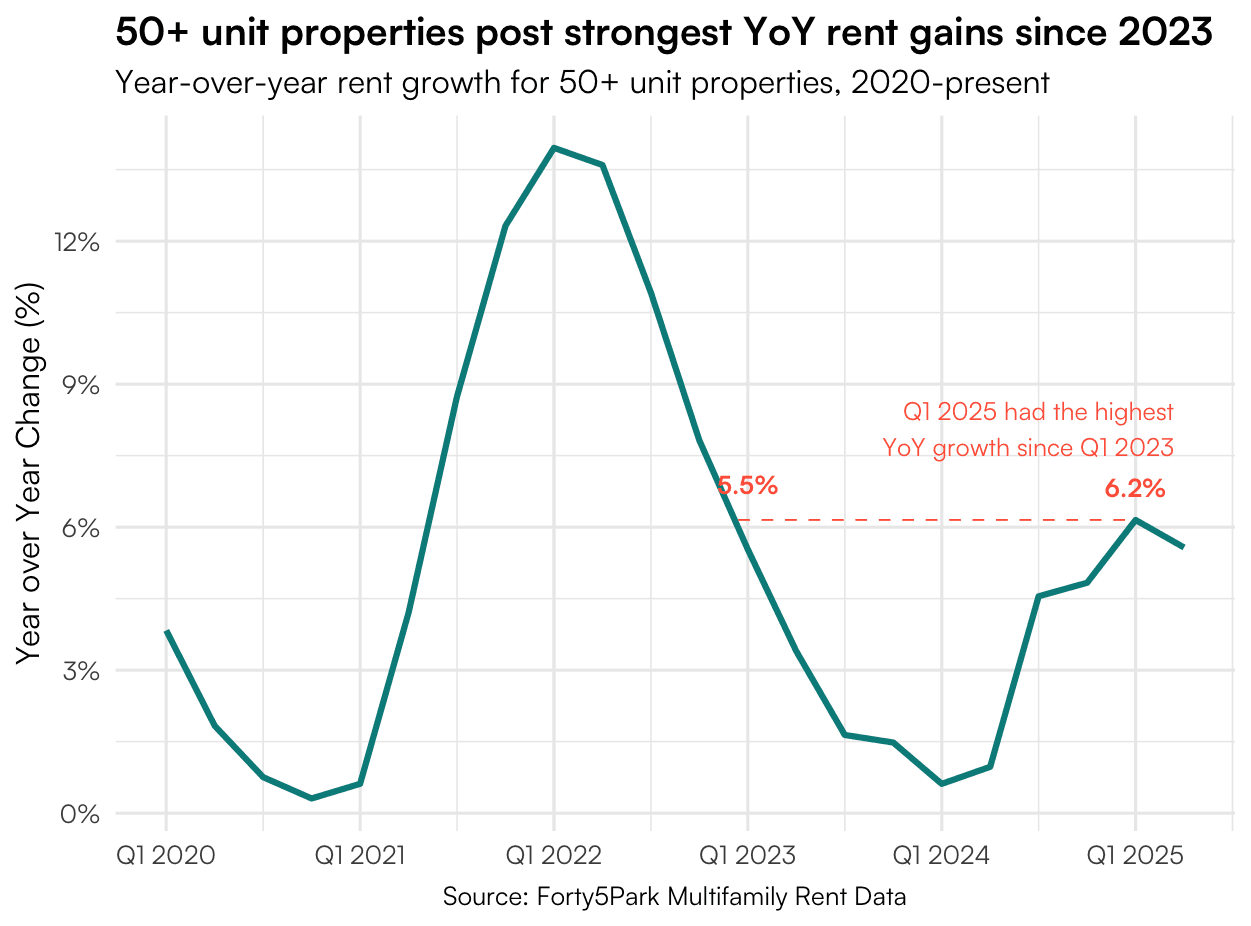

4. Accelerating Rent Growth

After nearly two years of weak performance, rent growth is showing clear acceleration signs. Average rent in our internal data increased 6.2% year-over-year in Q2 2025. This marks the highest rent growth in two years.

The trajectory is encouraging. Rent growth bottomed out at the end of 2024 and has been gradually improving throughout 2025 (CBRE). With slowing construction completions and healthy absorption continuing, rent growth is likely to strengthen further.

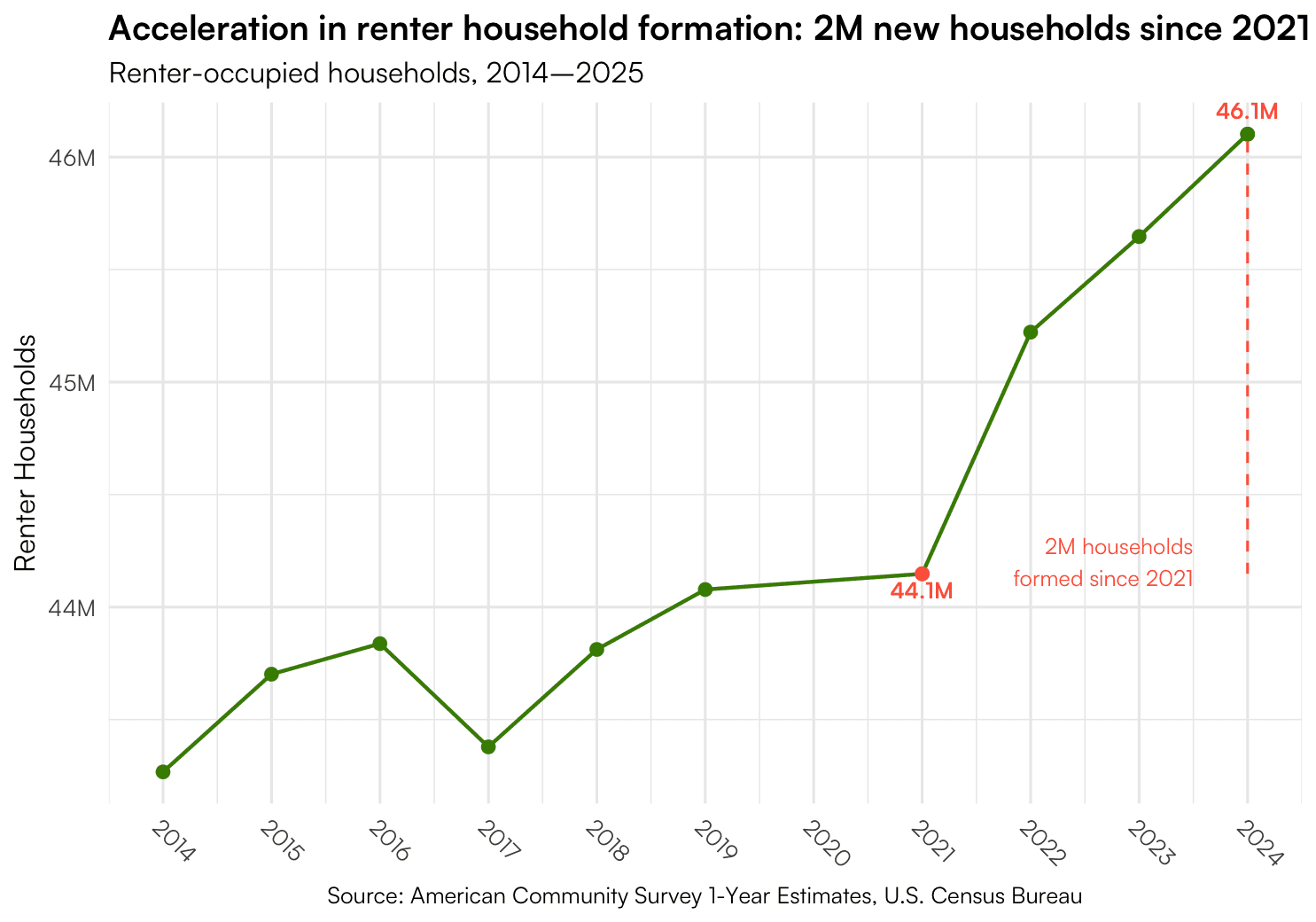

5. Record Renter Household Formation

The surge in renter demand isn’t a blip. Since 2021, the U.S. has added 2 million new renter households, marking the strongest acceleration in household formation in over a decade. With more households choosing to rent, the foundation of demand is deeper and more resilient than short-term market swings suggest.

In 2024 alone, rental households grew by 455k to reach 46 million: a 1.9% increase, more than double the growth rate of owner-occupied homes and the fastest pace since 2015 (U.S. Census Bureau). Renters now account for 35% of all occupied housing, the highest share since 2019.

The Bottom Line: Data Points to Strong Multifamily Returns

The evidence across all five indicators is clear: multifamily fundamentals are strengthening on multiple fronts. Absorption is running at record highs, vacancies are falling for the first time in a year, and supply is retreating just as demand accelerates. Rent growth has regained momentum, reaching its fastest pace in two years, while renter household formation has surged by 2 million since 2021, the strongest expansion in a decade.

This alignment of demand growth, tightening supply, and renewed pricing power is not noise in the data; it is the foundation of a new cycle. Risks like macroeconomic uncertainty and regional variation remain, but the core drivers of performance are firmly in place.

For investors and operators, the message is straightforward: the multifamily sector is ready to move beyond recovery.